It is never too early to start investing. In fact, the earlier you start, the better! Whether it be money saved since childhood, or a gift received from grandparents, it can be put to better use to help save perhaps for a car, an overseas trip, or even a deposit on a first home.

Investing an initial lump sum and then establishing a regular savings plan is a powerful way to grow your money by taking advantage of compound returns. It also establishes good habits by encouraging longer-term financial goals rather than spending without a considered plan.

Below are several options to consider, ranging from high-interest savings accounts to investing in shares and even extra superannuation contributions.

High Interest Savings accounts

Some banks offer high-interest savings accounts that pay a monthly bonus interest rate (as high as 5.25% per annum), typically requiring regular monthly deposits or regular withdrawals from a linked account.

For example, starting with $2,000 and contributing $100 per week could grow to approximately $32,000 in 5 years, and around $71,500 in 10 years:

")

")

Source: moneysmart.gov.au

The following link provides a comparison of the various options available. It is important to choose an account with no fees and consider any special conditions: Best High Interest Savings Accounts Australia 2026 | Canstar

Exchange Traded Funds (ETFs)

An Exchange Traded Fund (ETF) is like investing in one fund, holding a basket of shares. ETFs are listed on the Australian Stock exchange so they can be bought and sold, like individual shares. They also typically pay dividends, which you can often choose to reinvest automatically to continue growth. However, keep in mind there are costs to purchase each time, often around $20 per trade.

For example, ETFs may hold shares in the top Australian companies (including Telstra, Commonwealth Bank, BHP, etc.) or global markets (including Apple, Samsung, Tesla, Microsoft, etc.). There are many to choose from, therefore it is important to seek advice and check the underlying investment management fees.

While ETFs involve more risk, as values can fluctuate in the short term, they also offer the opportunity for greater returns if you are prepared to keep the money invested for a longer term – ideally 7+ years. That’s not to say you can’t access it before then, you just need to allow time to average out any market fluctuations.

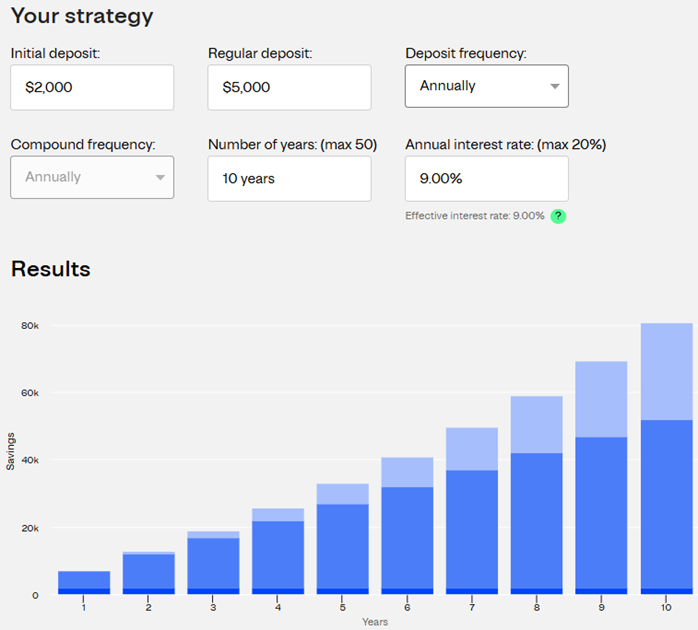

For example, over the last 20 years, the Australian share market has returned between 8% and 10% per year. Therefore, investing $2,000 and adding $5,000 each year could grow to approximately $80,000 over 10 years (including reinvested dividends).

Source: moneysmart.gov.au

Micro-investing

There are also platforms or apps available, referred to as “micro-investing,” where you can start with as little as $100. You can add small amounts to it over time. While accessible and convenient, they often come with relatively high fees, so it’s important to assess whether they suit your needs.

Another strong option is to start contributing to super when young adults start their first full-time job, yet it’s often overlooked due to its inaccessibility until at least age 60. However, starting early can make a significant difference in the long run.

For example, contributing $100 per fortnight from age 18, alongside an employer contribution of 12% on a $60,000 salary, could result in a super balance almost $190,000 higher by age 60! That’s without even considering wage increases. The other benefit is that if you ask your employer to make these contributions before tax, there is a tax saving of $32, so the net fortnightly pay you receive will only reduce by $68.

We believe it is so important for young adults to embrace financial literacy at an early age, therefore our advisers are happy to assist your children or even grandchildren to help them instil good habits and appreciation for money as early as possible.